In South Carolina in 2025, Big Insurance Corporations have launched an unprecedented effort to make it harder for individual consumers to recover from their insurance companies when bad things happen to them. Conservatives need to stand up and call their legislators to make their voices heard.

In South Carolina in 2025, Big Insurance Corporations have launched an unprecedented effort to make it harder for individual consumers to recover from their insurance companies when bad things happen to them. Conservatives need to stand up and call their legislators to make their voices heard.

Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!

Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!Donald Trump Jr. and MAGA America are weighing in to oppose S.244 and this Bailout to Big Insurance!

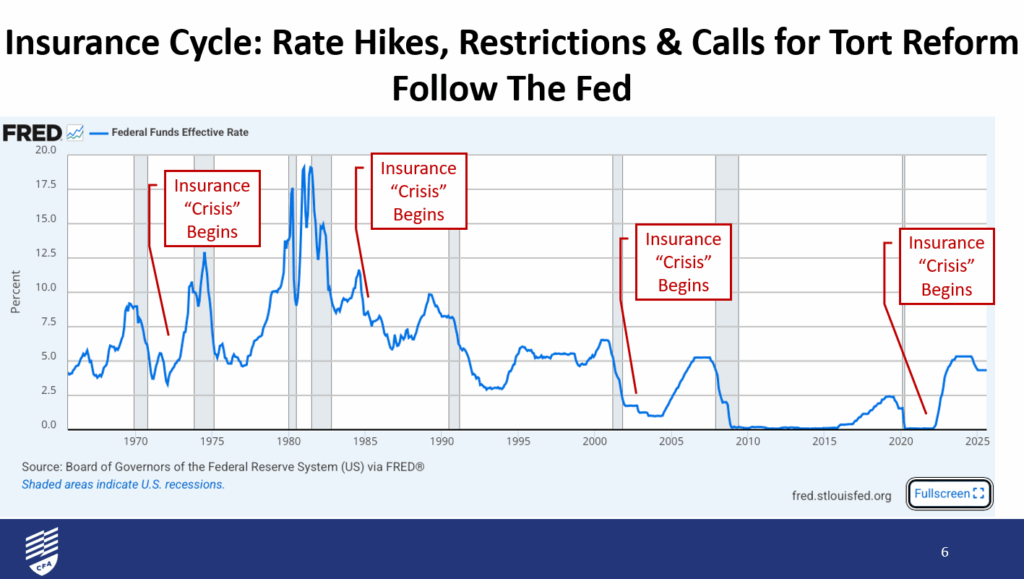

Political pressure rises (often including calls for “tort reform”).

Then markets loosen later—but consumer prices don’t always fall quickly.

Doug Heller’s presentation framed this as a repeating pattern: rate hikes + restrictions + calls for tort reform often follow changes in interest rates.

B) Premiums aren’t only about storms—pricing choices matter

Even when claim frequency isn’t the highest, premiums can still rise because insurers:

change underwriting rules,

reshape who they want to insure,

and use pricing factors that aren’t directly about roof strength or driving safety.

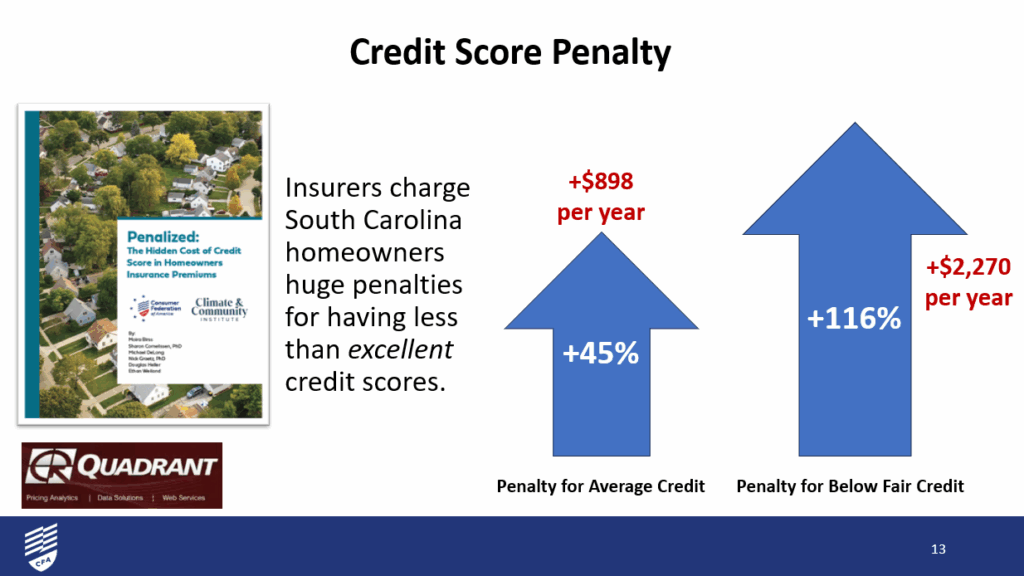

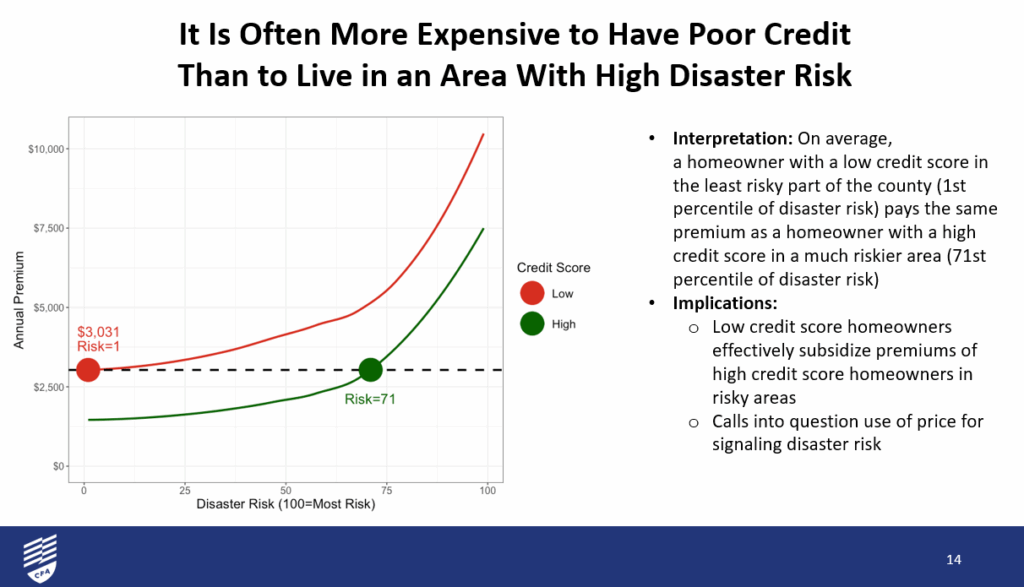

C) Credit score penalties can overwhelm “real risk”

Doug Heller’s presentation shows that insurers can charge huge penalties for less-than-excellent credit for homeowners insurance in South Carolina:

Average credit: about +45% (about +$898/year)

Below fair credit: about +116% (about +$2,270/year)

It also highlights an important comparison: it can be more expensive to have poor credit than to live in a higher-disaster-risk area, meaning pricing may reflect financial profiling more than hazard risk.

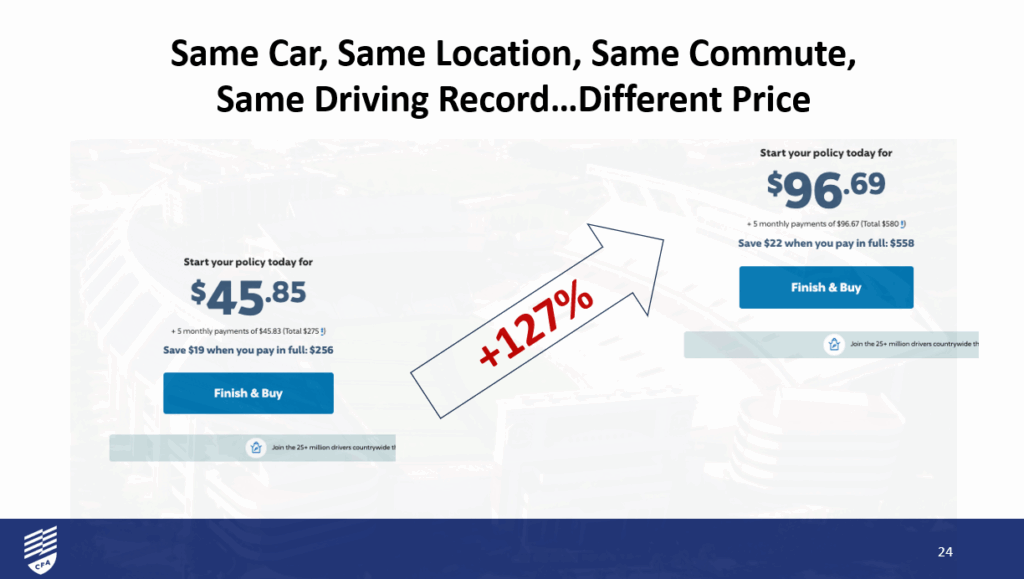

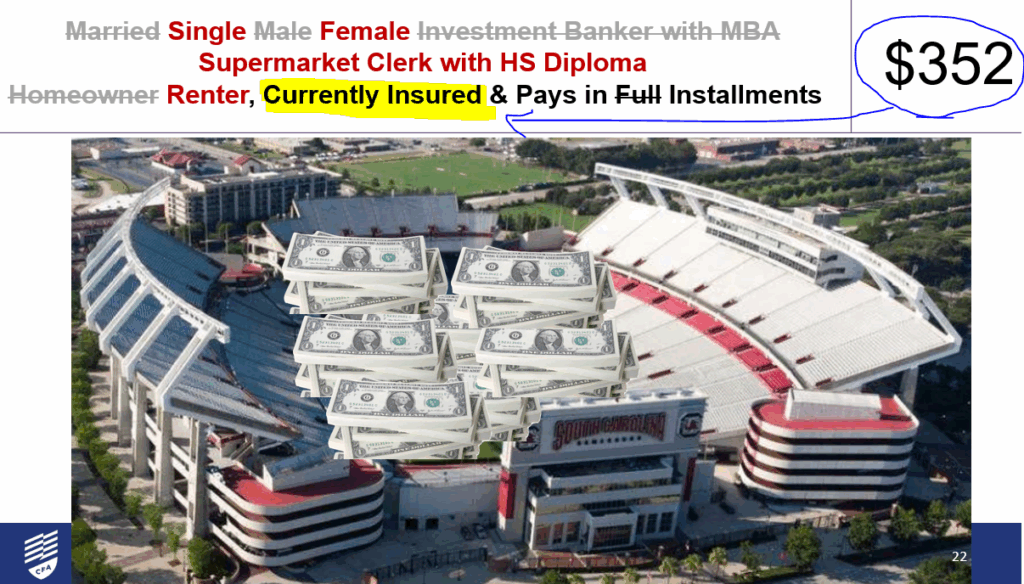

D) Auto premiums can vary wildly for the same safe driver

Heller’s example uses a single 35-year-old driver in Columbia with the same car, commute, and perfect driving record—yet the price changes when you modify socioeconomic descriptors (marital status, education, occupation, renter vs homeowner, pay-in-full vs installments, lapse in coverage). In his example, the quote rises from $256 to $580 for six months—a +127% increase—without changing driving risk.

E) When people are forced out of coverage, the whole system gets worse

As premiums rise, more households go uninsured. The presentation reports:

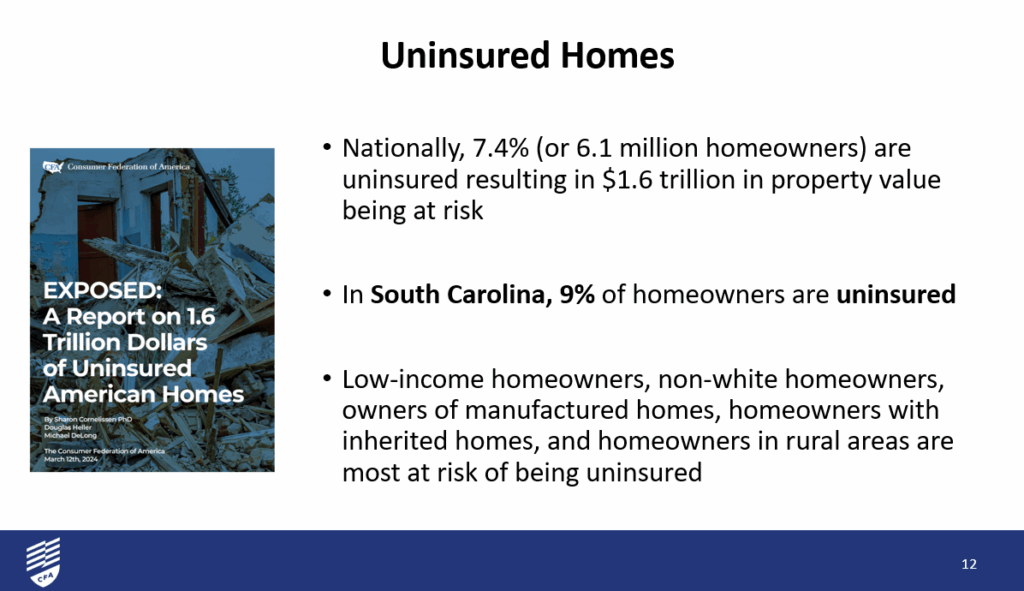

Nationally: 7.4% of homeowners uninsured

South Carolina:9% of homeowners uninsured

When fewer people can afford coverage, risk becomes less broadly shared—and communities hit by disasters may not rebuild, which can create neighborhood decline and long-term economic harm.

3) “Myths vs Facts”

Myth: “Rates are high because insurers are barely breaking even.”

Fact: Underwriting results go up and down, but the overall business model includes investment earnings and pricing lag. The presentation also points to strong recent industry profits and large shareholder payouts in 2024.

Myth: “If we restrict insurers, they’ll all leave.”

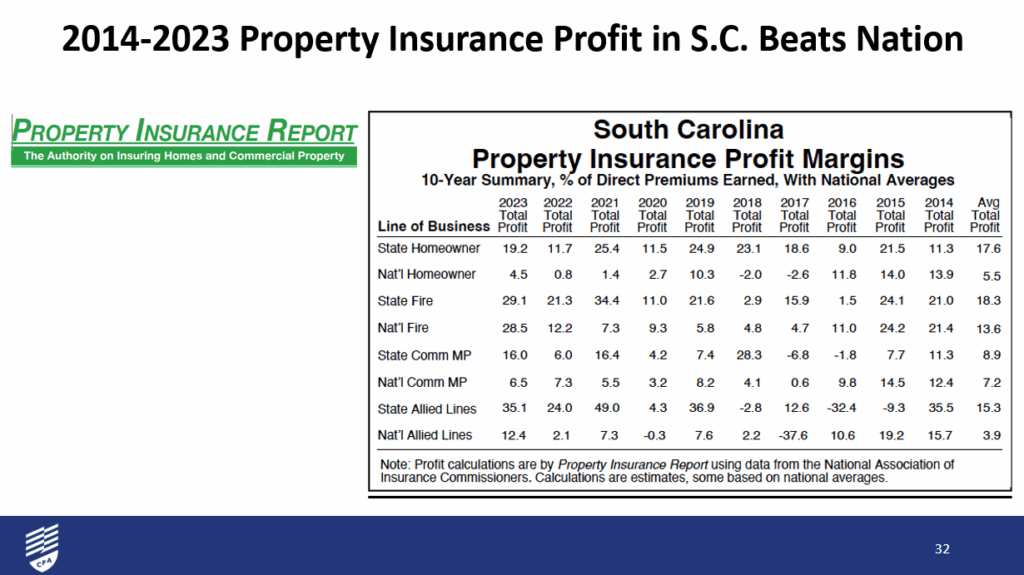

Fact: Doug Heller argues insurers often threaten to leave, but also shows insurers operating in South Carolina can post strong results compared to national averages in multiple lines.

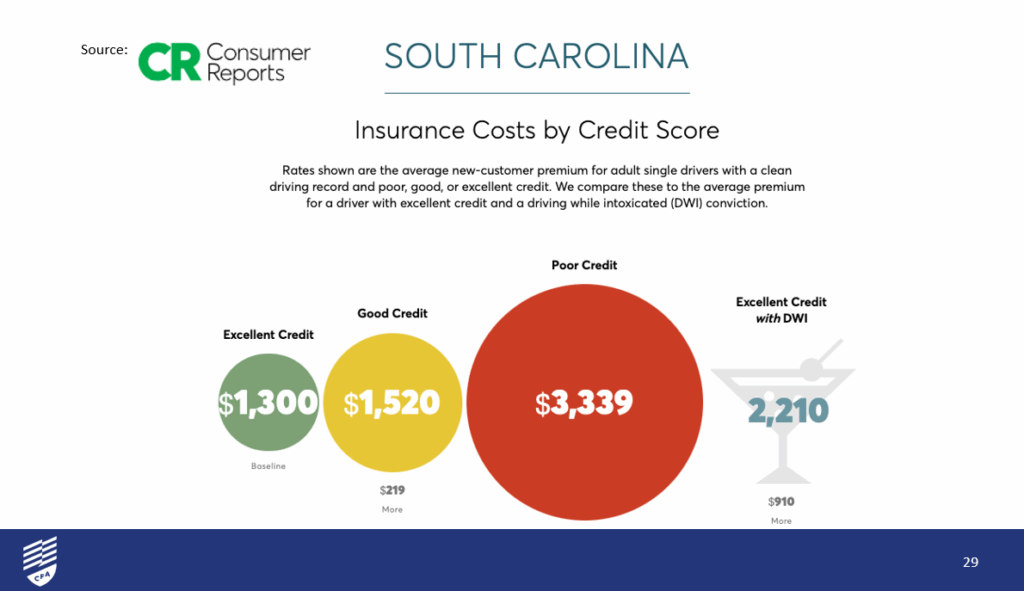

Myth: “Your premium mostly reflects your roof or your driving.”

Fact: Pricing can be heavily influenced by factors like credit-based insurance scores and other non-driving/non-roof socioeconomic characteristics. A driver with a perfect driving record but poor credit score pays more than an individual with excellent credit and a DWI.

Myth: “Advertising doesn’t affect my bill.”

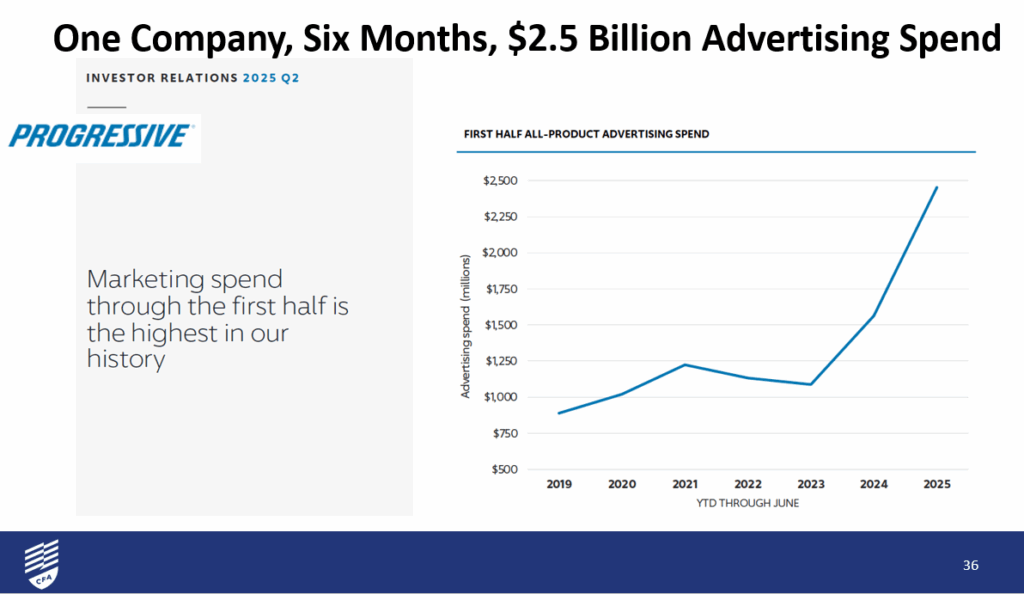

Fact: Doug Heller’s presentation highlights one major insurer spending about $2.5B on advertising in six months, which is paid from premium dollars as part of insurer expenses.

4) Practical consumer guidance page (what you can do now)

If your home premium jumped

Shop and re-shop (especially at renewal).

Ask the agent: “Are you using credit-based insurance scoring, and is there any option less dependent on credit?”

Request higher deductibles only if you can truly afford them after a disaster.

Check for discounts you’re eligible for (wind mitigation, roof updates, bundling—only if it truly saves money).

If your auto premium jumped

Avoid a lapse in coverage if at all possible (the presentation’s example shows this can trigger very large increases).

telematics (only if you’re comfortable with tracking).

If you’re thinking about going uninsured

Understand the community impact: uninsured homes after storms can mean fewer rebuilds and more blight.

If cost is the barrier, ask about:

reduced coverage options (not ideal, but better than zero),

payment plans,

local mitigation grants/roof help (if available).

(This section is educational, not legal or financial advice.)

5) What lawmakers can do to lower premiums without shifting costs onto families?

Policies to consider to protect consumers

More transparency and data: fund the capacity to collect and analyze rate/claims/pricing data so regulators and researchers can test what’s driving increases.

Guardrails on credit-based pricing: consider limits or prohibitions (the deck notes some states prohibit credit scoring in homeowners).

Clarify “unfairly discriminatory”: define what should not be used (or how it must be justified) to prevent economic profiling.

Monitor affordability and access: track non-renewals, uninsured rates, and availability gaps by county/ZIP, especially rural and manufactured housing areas.

Conclusion Doug Heller’s presentation makes clear that high insurance premiums in South Carolina are not driven by a single factor, but by a combination of insurance market cycles, pricing choices, and the growing use of financial and socioeconomic factors that can outweigh actual risk. When premiums rise faster than incomes, more families are pushed out of coverage, weakening the insurance pool and harming communities as a whole. Addressing affordability will require transparency, data-driven oversight, and consumer protections that focus on how insurance is priced—not just how insurers explain it.